From recharge portals to payment systems, digital gold, loan journeys, and API services, the plug and play fintech model allows companies to launch new services instantly without building everything from scratch.

In this blog, we break down the plug and play meaning, benefits, use cases, and why it’s becoming the backbone of modern fintech platforms.

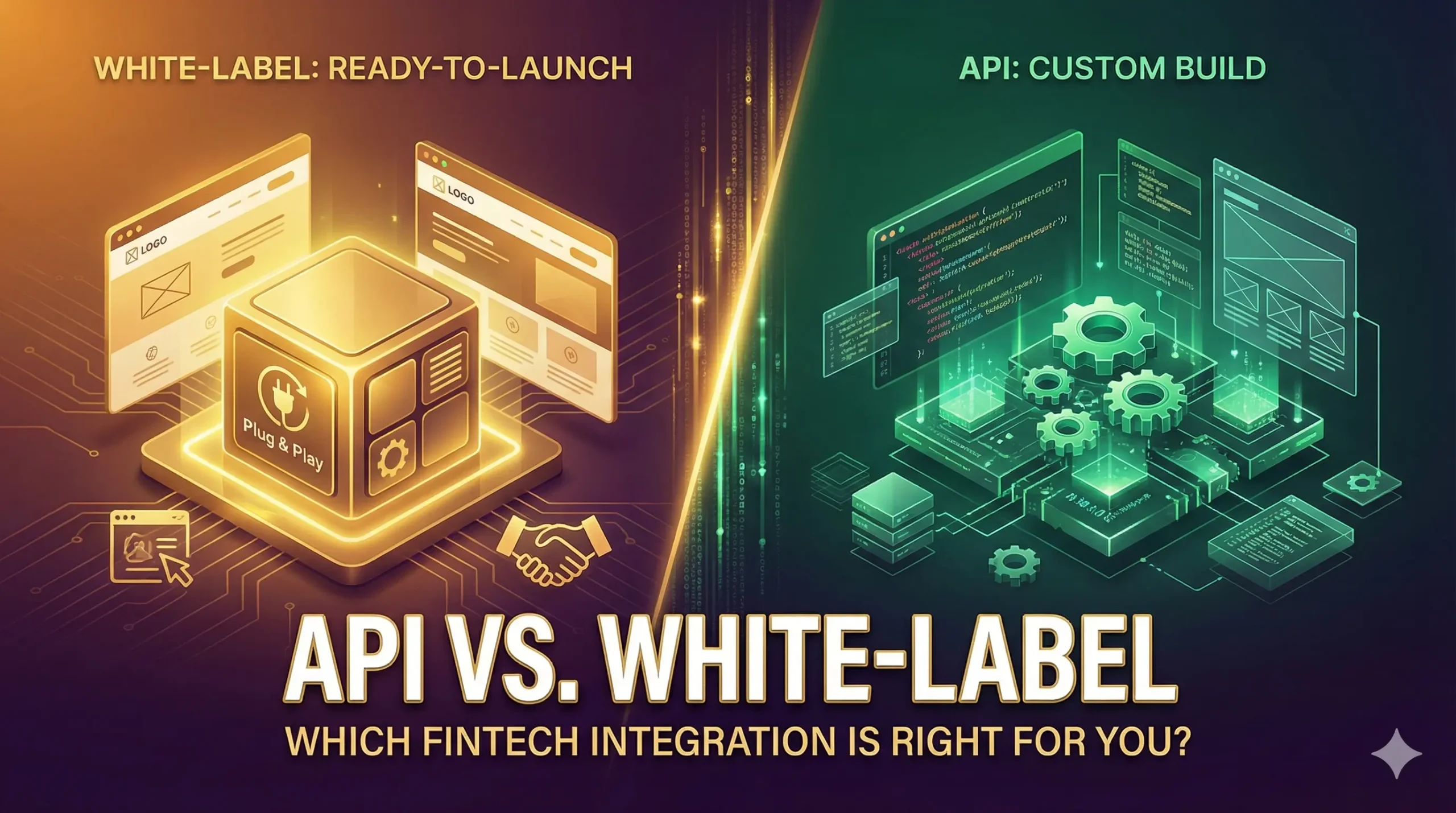

What Is Plug and Play?

A ready-made system that works instantly once connected — without the need for complex setup, coding, or development.

Originally used for computer hardware, today the concept is widely used in software and fintech platforms.

Plug and Play Meaning in Fintech

In fintech, plug and play meaning refers to: A pre-built fintech platform with all integrations, APIs, features, UI, backend, and compliance already ready — allowing businesses to launch instantly.

You don’t need:

❌ Developers

❌ Expensive tech teams

❌ Long development cycles

❌ API negotiations

❌ Compliance setups

Everything is pre-built. You simply plug it in and start operating.

What Is a Plug and Play Fintech Model?

The plug and play model in fintech works like this:

The provider (like Inditab) builds a complete fintech infrastructure.

Partners can instantly activate services such as:

Recharge & bill payments

Digital gold & silver

Travel bookings

DMT & AePS

Gift cards

PAN & utility services

Credit & loan journeys

Partners get a ready dashboard, admin panel, APIs, payout system, wallets & settlement modules.

The business goes live within 24–72 hours.

This helps entrepreneurs, fintech startups, and enterprises launch quickly without investing crores in development.

Why Plug and Play Fintech Solutions Are Gaining Popularity

1. Zero Development Cost

No need to hire developers or build a system from scratch.

2. Go Live Within Days

Instead of 6–12 months, your platform can launch within a few hours or days.

3. Fully Tested System

All bugs, load testing, UI improvements, and security layers are already validated.

4. 100% Scalable

The plug and play model grows as your customer base grows.

5. Compliance Is Handled

API licensing, KYC rules, settlement norms, and regulatory tasks are already managed.

6. Support & Maintenance Included

No need to run your own tech support team.

Popular Use Cases of Plug and Play in Fintech

1. Bill Payment & Recharge Portals (BBPS & APIs)

Businesses launch a recharge/bill payment platform instantly.

2. Digital Gold & Silver Platforms

Ready-made modules for buying, selling & storing digital gold.

3. Loan & Credit Application Journeys

AI-based journeys for:

Credit cards

Personal loans

Business loans

NBFC/Bank integrations

4. Whitelabel Travel Booking Platform

Flight & hotel booking modules with instant commissions.

5. DMT, AePS & Micro-ATM Setup

Designed for retailers, DSAs, and B2B fintech aggregators.

Benefits for New Entrepreneurs & Startups

Launch a fintech business without technical knowledge

Start earning from day one

Low investment, high returns

Build a brand instantly using a whitelabel setup

Scale to more services as you grow

The plug and play fintech model removes all barriers for entrepreneurs who want to enter the profitable fintech space.

Why Plug and Play Is the Future of Fintech

With India moving towards digital-first services, the demand for:

✔ Ready-made fintech infrastructure

✔ Instant API connectivity

✔ Faster GTM (Go-To-Market)

✔ Low-cost business setup

…is increasing rapidly.

The plug and play model ensures that businesses don’t lose time or money building tech, and instead focus on acquiring customers and growing revenue.

Final Thoughts

The plug and play fintech model is revolutionizing how companies launch fintech solutions. Whether you’re a startup, retailer, entrepreneur, or enterprise — adopting a plug and play approach helps you:

Launch faster

Reduce costs

Minimize risk

Scale easily

Offer multiple digital services under one platform

If you’re planning to enter the fintech industry, plug and play solutions are the smartest, fastest, and most cost-effective way to start.